Fixed Expenses: 3 Reasons They Are Killing Your Wealth

Fixed expenses are the true “silent wealth killers” in modern budgets. In 2024, the average American household expenditure climbed to $78,535, and

while the common financial narrative fixates on “small leaks”—the $5 latte or the $15 avocado toast—the data tells a different story.

This isn’t a discretionary spending problem; it’s a structural one. These recurring, predictable obligations remain consistent regardless of your lifestyle

activity or economic health. As the foundational bedrock of your budget, fixed expenses encompass everything from mortgage payments and insurance premiums to the high-speed internet that powers your career.

While these provide a predictable baseline for financial planning, they simultaneously create a high “burn rate” and dangerous financial “rigidity.”

When your fixed obligations consume too much of your income, you lose operational leverage. You aren’t building wealth; you are simply servicing a

break-even point that demands constant, unrelenting revenue just to keep the lights on.

Some blogs of other website are given below

Average American household expenditure 2024: $78,535

Official source: U.S. Bureau of Labor Statistics (BLS) Consumer Expenditure Survey 2024. → BLS News Release

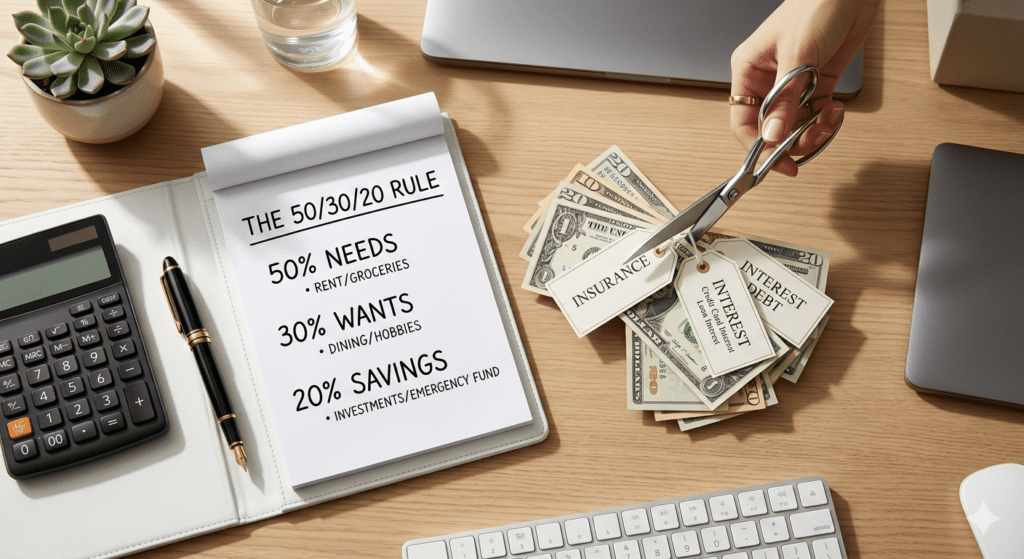

The 50/30/20 Framework and the “Concrete Block”

The 50/30/20 rule is often treated as a financial law: 50% of income toward “needs,” 30% to “wants,” and 20% to savings.

However, this framework fails when the “needs” column becomes an unyielding concrete block of fixed costs.

For many, these “needs” are actually choices houses that are too large or car payments that are too heavy disguised as necessities.

To achieve fiscal mastery, you must view every dollar of recurring expense through the lens of a commercial strategist.

The Revenue Multiple Mental Model In strategic finance, every dollar of fixed expense requires a specific revenue multiple to sustain.

For an individual, a $100 increase in a monthly subscription doesn’t just cost $100;

due to the friction of income taxes and the necessity of maintaining profit (savings) margins, it may require $125 to $150 in gross earnings to offset.

Lowering your fixed baseline is the most efficient way to increase your financial “elasticity.”

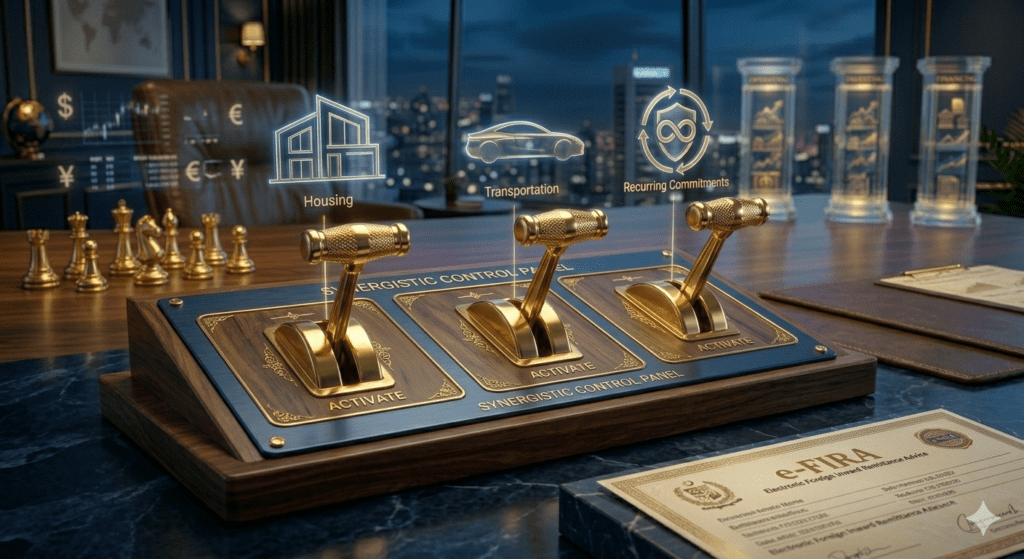

The “Big Three” Fixed Cost Levers

To move the needle on wealth, you must target the three categories that consume the lion’s share of most budgets.

1. Housing: Your Largest Opportunity

Housing remains the single most significant fixed obligation, consuming approximately 33.4% of the average budget. In 2024,

median gross rent surged by 36% compared to 2019 levels, and mortgage renewals have seen average payment spikes of nearly $457.

Because of this scale, housing offers the greatest optimization dividend:

- Strategic Relocation:

- Transitioning to more affordable markets or downsizing can structurally reset your burn rate.

- Assessment Challenges:

- Property taxes are not set in stone; challenging local assessments to prove a home’s value is lower than estimated can lead to permanent annual savings.

- The Refinance Window:

- In falling-rate environments, or as your credit profile improves, refinancing can shave hundreds off your monthly baseline.

2. Transportation: Beyond the Car Payment

Transportation accounts for roughly 17% of the average budget, often driven by the “lifestyle creep” of luxury vehicle leases.

- The Cash-and-Upgrade Model: Buy the most reliable vehicle you can afford with cash.

- Immediately begin “paying yourself” a car payment into a dedicated account. When it is time to upgrade,

- sell the current vehicle and add the accumulated cash to buy the next one outright.

- This eliminates the 20% interest-rate trap common in subprime auto lending.

- Public Transit as an Alternative:

- In high-density cities, switching to public transit can eliminate maintenance,

- insurance, and the 7% of income many consumers lose to energy/fuel costs.

3. Debt and Interest: The Non-Negotiable Drain

With the average consumer carrying $21,296 in debt and mortgage delinquency rates soaring by over 135% in certain regions, interest has become a structural parasite.

“Interest payments provide zero operational or personal value. They are the ultimate ‘ghost cost’—money that vanishes without providing utility, comfort, or assets.”

Prioritize debt consolidation via 0% APR balance transfer cards or personal loans to convert high-interest variable debt into a single, predictable, and rapidly amortizing fixed payment.

The “Silent Spenders”: Subscriptions and Micro-Fixed Costs

Modern budgets are plagued by “automation bias.” Small, recurring digital fees go unquestioned, creating a cumulative drag on your capital.

Perform a “Subscription Scrub Down” of your statements and look specifically for:

- The Storage Unit Trap: 10% of Americans rent offsite storage. In almost every case, this is an unnecessary fixed cost for items that have likely depreciated to zero.

- Underused “Pro” Software: For the digital entrepreneur, recurring licenses for SEO tools like Ahrefs/Semrush or design suites like Adobe must be re-justified every six months.

- Streaming Overlap: Prune services like Netflix or Disney+ if they are no longer providing active entertainment value.

- The Cable Trade-off: Ditching traditional cable for leaner streaming bundles remains one of the fastest ways to reclaim monthly cash flow.

The Middle-Class Strategy: Optimization Over Deprivation

For the middle class, especially in emerging markets like India, certain fixed costs are actually “Fixed Investments.”

In metropolitan hubs like Mumbai or Bengaluru where a comfortable life for a family of four can cost between ₹2,70,000 and ₹4,50,000 per month domestic

help (ranging from ₹3,000 to ₹18,000) is a strategic enabler. These are “operational expenses” that allow dual-income households to focus on higher-revenue activities.

Strategic optimization is about the intentional selection of these burdens.

Category | Fixed Optimization Tactic | Impact |

Insurance | Bundling Home/Auto & Annual Policy Checks | Structural Dividend: Up to 25% Savings |

Utilities | Energy-efficient appliances & Even-Pay plans | Stability: Mitigates the 7% income drain on energy |

Cell/Internet | Renegotiating contracts/Removing overages | Immediate Gain: 10-15% Monthly reduction |

Childcare | Neighborhood research & program enrollment | Structural Reduction: Significant baseline shift |

The OBBBA 2025 Advantage

For freelancers and digital entrepreneurs, the One Big Beautiful Bill Act (OBBBA) of 2025 offers powerful new levers.

Purchases made after January 19, 2025, qualify for 100% bonus depreciation, allowing you to immediately deduct the full cost of business equipment (computers, studio lighting, cameras).

Furthermore, self-employed individuals can now deduct 100% of health insurance premiums from their taxable income, turning a massive fixed burden into a major tax advantage.

Long-Term Wealth: Compounding Through Consistency

Lowering your “burn rate” isn’t about austerity; it’s about freeing the capital needed for the 20–30% investment rule.

By automating a Systematic Investment Plan (SIP) such as the ₹11,000 monthly contribution that can build a ₹2 Crore corpus over time you turn today’s reduced expenses into a future “income floor.”

For those nearing retirement, fixed index annuities with living benefits can provide a guaranteed base of income.

These tools offer the potential for growth tied to market indices while ensuring your core fixed expenses are covered by a dependable income floor, regardless of market swings.

Conclusion: Redefining Your Financial Baseline

Fiscal mastery is the result of the intentional selection of your fixed burdens. Every fixed cost you optimize or eliminate is a permanent,

tax-free raise you give yourself every single month. Look at your budget and ask yourself this reflection question:

“If your income disappeared tomorrow, how many months would your current fixed costs allow you to survive?”

If that number is uncomfortably low, you must act. Within the next 48 hours, perform your first “Fixed Cost Scrub Down.

” Cancel one unused subscription, call one insurance provider to bundle your policies, and review your eligibility for the OBBBA 2025 deductions. Your future wealth depends on the margin you create today.

Pingback: Complete Guide to Cash Flow Management forSmallBusinesses