Freelancer & Small Business Finance: 7 Essential Secrets to Master Your Money in 2025

1. Introduction: The High Cost of Financial Ignorance

Mastering freelancer & small business finance is the only way to break the “feast-or-famine” cycle that traps most self-employed professionals. For many, the difference between paying ₹0 tax and ₹4 lakh isn’t a matter of luck—it’s a calculated application of the tax code. In 2025, an Indian freelancer earning ₹24 lakh can legally pay zero income tax, while their less-informed peers may lose nearly 15% of their gross revenue to the government.

Irregular income and poor cash flow management are the leading causes of small business failure. Without a structured framework, recurring costs often outpace revenue, and unpaid invoices quietly drain the business’s lifeblood. This guide provides an authoritative, ITD/IRS-compliant roadmap to automate your savings, optimize your tax structure, and protect your hard-earned income.

our other posts are given below

our other posts are given below

2. Basic Concepts: The Foundation of Your Business Ledger

Managing freelancer & small business finance begins with absolute clarity regarding your business’s value. To move beyond basic bookkeeping, you must understand the three core components of a balance sheet, as defined by the SBA and GAAP standards:

Component | Definition | Examples |

Assets | What your business owns | Cash, equipment, inventory, accounts receivable |

Liabilities | What your business owes | Business loans, accounts payable, credit card debt |

Owner’s Equity | Your ownership stake | Assets minus Liabilities (the value you actually hold) |

Choosing an Accounting Method

How you record these components depends on your accounting method:

- Cash Basis Accounting: Transactions are recorded only when cash changes hands. This is simpler for micro-businesses as it reflects actual cash on hand.

- Accrual Basis Accounting: Transactions are recorded when they are earned or incurred, regardless of when the payment is made. This provides a more accurate long-term picture of profitability and is required for larger businesses or those maintaining significant inventory.

3. Mastering the Tax Regimes: Section 44ADA and the Zero-Tax Secret

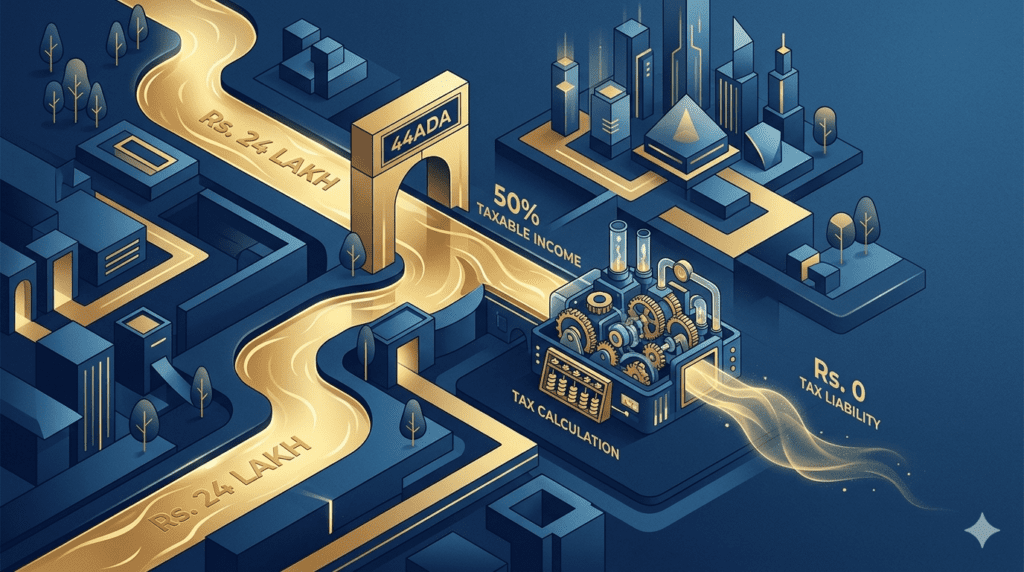

The most transformative secret in freelancer & small business finance is the “₹24 Lakh Zero-Tax” strategy. By leveraging the interplay between Section 44ADA and the New Tax Regime (FY 2025-26), eligible professionals can eliminate their tax liability entirely.

The Math of the ₹24 Lakh Secret:

- Section 44ADA (Presumptive Taxation): If you are a professional (IT consultant, writer, designer, etc.) with gross receipts up to ₹75 lakh (where 95%+ of receipts are digital), you can declare only 50% of your income as profit.

- Calculation: Gross ₹24,00,000 → 50% Taxable Income = ₹12,00,000.

- Section 87A Rebate: Under the New Tax Regime, the 87A rebate applies to taxable income up to ₹12 lakh.

- Result: Net Tax Liability = ₹0.

The HUF Income-Splitting Mechanism

A Hindu Undivided Family (HUF) is a separate legal tax entity with its own PAN and tax slabs. The “secret” here is income splitting: by shifting income from ancestral property or collective family efforts to an HUF, you utilize a second basic exemption threshold (₹4 lakh under the new regime). This effectively allows a freelancer to split their total income across two entities, potentially saving an additional ₹1–3 lakh annually.

US Tax Considerations

For those with US-based clients, the stakes are equally high. You face Self-Employment Tax (15.3%) for US-source income, while missing documentation can trigger 24% Backup Withholding or 30% Statutory Nonresident Withholding.

our other posts are given below

our other posts are given below

4. The “Silent Killers”: Why Cash Flow Fails

Financial failure is rarely a single event; it is the result of cumulative, unaddressed “silent killers”:

- The 1% Penalty Trap: Failing to pay Advance Tax on time triggers interest penalties under Sections 234B and 234C. This is a 1% monthly interest charge on the unpaid amount.

- The Foreign Remittance Mismatch: Foreign inward remittances often do not appear in Form 26AS. If your declared income doesn’t reconcile with the bank records visible to the ITD, you risk a scrutiny notice under Section 143(1).

- Poor Collection Habits: Unpaid invoices are the primary cause of insolvency. You must treat invoice aging with the same urgency as your primary work.

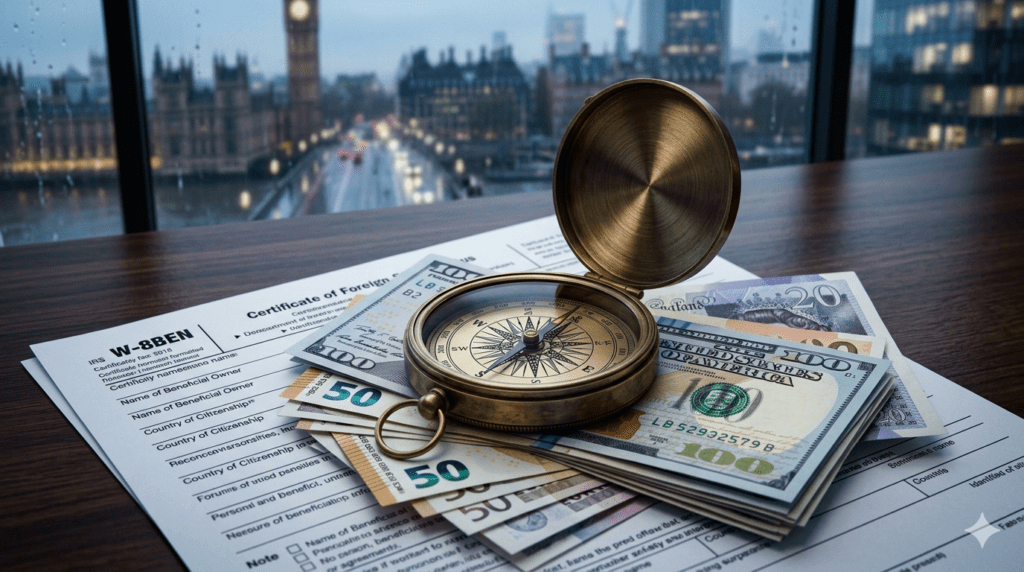

5. Navigating International Compliance: W-8BEN and Foreign Source Income

For Indian freelancers working on platforms like Upwork or YouTube, the W-8BEN form is a critical tool to reduce US tax withholding.

The key distinction is Foreign Source Income. Services performed entirely in India are considered foreign-source by the IRS. With a valid W-8BEN, the withholding on these services drops from 30% to 0%. However, royalties (like YouTube AdSense from US viewers) are taxed at the treaty-reduced rate of 15%.

To protect your income, you must explicitly include the phrase “Services performed in India” on all contracts and invoices. This documentation, combined with your W-8BEN, ensures you aren’t paying the US for work done in Bengaluru or Mumbai.

our other posts are given below

our other posts are given below

6. The Step-by-Step Financial Mastery System

- Strict Separation: Open a dedicated business bank account immediately. This prevents “piercing the corporate veil,” which could otherwise make your personal assets liable for business debts.

- The 70/20/10 Rule: Allocate 70% of revenue to operating expenses, 20% to savings or debt repayment, and 10% to personal compensation or growth. Alternatively, use the 50/30/20 model (Operations/Growth/Development).

- Tax Reserve Strategy: If you use Section 44ADA, remember that your entire Advance Tax is due in a single installment by March 15.

- Operating Buffer: Build a cash reserve of 3 to 6 months of operating expenses to survive the feast-or-famine cycles inherent in freelancing.

7. Essential Tools and Resources for 2025

Modern freelancer & small business finance requires automation. Based on technical performance and scalability, we recommend:

- QuickBooks Online: The industry standard for depth, customizability, and inventory management.

- Zoho Books: Best for larger small businesses and midsize companies needing deep flexibility and multi-user support.

- Xero: Ideal for businesses requiring unlimited users and powerful employee expense management tools.

- FreshBooks: Excellent for service-based freelancers who prioritize project management and time tracking.

Compliance Platforms:

To manage foreign currency (USD, GBP, EUR) with competitive FX rates, use platforms like Karbon Business or Winvesta. These tools automatically generate the e-FIRA (Foreign Inward Remittance Advice) required for FEMA and tax compliance in India.

our other posts are given below

our other posts are given below

8. Common Mistakes to Avoid

- Mixing Credit Lines: Using personal credit cards for business hardware obscures your true overhead and complicates home office deductions.

- Ignoring Documented Expenses: If you exceed the ₹75 lakh limit and cannot use presumptive taxation, you must have a formal rent agreement and your landlord’s PAN to claim home office deductions (proportional rent/electricity).

- Expired Tax Forms: A W-8BEN is valid for only three calendar years. If you fail to renew it, platforms will retroactively apply 24% backup withholding to your payouts.

Conclusion: Your Compliance Checklist

To keep your freelancer & small business finance secure, follow this “Before July 31” checklist:

- Reconcile 26AS/AIS: Ensure all TDS credits and inward remittances match your internal records.

- Verify 44ADA Eligibility: Confirm gross receipts are below ₹75 lakh and 95%+ are digital.

- Choose the Correct Form: Use ITR-4 for presumptive (44ADA) income. If you maintain actual books or exceed the turnover limit, use ITR-3.

- Collect e-FIRCs: Gather all certificates for foreign payments to prevent ITR mismatches.

- Audit Advance Tax: Ensure 100% of your liability was paid by March 15 to avoid the 1% monthly penalty.

Final Call to Action: Treat your finances as a core business process. Schedule a “Financial Health Day” once a month to review your profit and loss statements and adjust your pricing strategy to maximize your margins.